Here you will find interesting quotes, useful information and links to helpful articles on a wide variety of subjects.

Julie's Blog Posts

Quote of the Week

Behaviour versus everything else!

There are a lot of people running around out there making a lot of noise and waving their hands, trying to tell you what you should be focusing on as an investor.

These “hand-wavey'' people talk about China, things like the Reserve Bank, monetary policy, stimulus, asset allocation, cryptocurrency, and shiny objects like silver and gold. It’s an awful lot to keep track of.

And don’t get me wrong, some of those things actually do matter. It’s not a bad idea to learn about them.

But one thing is certain: When it comes to investing, nothing matters anywhere near as much as your behavior.

You can design the greatest portfolio ever created by humankind, and one behavioral mistake a decade could mean you would've been better off in a bank account or stuffing the cash in your mattress.

So yes, the economy matters, smart portfolio design matters, how much we have in small cap, value, and growth, all those things matter.

But the thing that matters most is having investments that will allow you to behave.

In fact, I would argue that even portfolio design only matters to the degree that it influences good behavior.

Arguing over whether you should have 17.2% or 17.5% in emerging markets might be an interesting debate, but the difference between 17.2 and 17.5 is a misdemeanor when the felony we’re all committing is behaving poorly.

So next time a “hand-wavey” person shows up in your face telling you all the things you should be doing, just smile, nod, and walk away.

And remember that none of it matters if you don't know how to behave.

Blog written by Carl Richards from Behaviorgap.com :-)

Australia's new government - what does it mean for investors?

A big change to the political landscape has occured with the change of government. So where to from here for us investors? What changes may occur that will impact on you? I read a great overview from Shane Oliver at AMP Capital recently... click on the below link to take a peek.

Investment performance and start date randomness

When it comes to your inception date with an investment advisor, chance plays a huge role.

The same goes for investment strategies going in or out of favour. Warren Buffett, the greatest investor of all time, has had multiple, prolonged periods of underperformance. His style was out of favour, but he stuck to it. And once again, he is reaping the rewards of his discipline. Berkshire Hathaway stock is up 18% year to date while the market is down 5%. So too does any investment style go in or out of favour. Ours is no exception.

Keep reading here for a great article about start dates: https://www.firstlinks.com.au/investment-performance-start-date-randomness

Quote for the Week!

The escalation in Ukraine tensions - implications for investors

- Share markets are at high risk of more downside on fear of further escalation and uncertainty about sanctions/gas supply to Europe.

- The history of crisis events shows a short term hit to markets followed by a rebound over 3 to 12 months.

- Given the difficulty in timing market reactions to geopolitical developments the best approach for most investors is to stick to an appropriate long term investment strategy.

Read the attached synoposis from Shane Oliver - Chief Economist from AMP .

Happy New Year from the Team!

Jenny, Julie, Robyn, Deborah & Hotch the Whippet wish you all the best for a restful and happy festive season.

See you all in 2022.

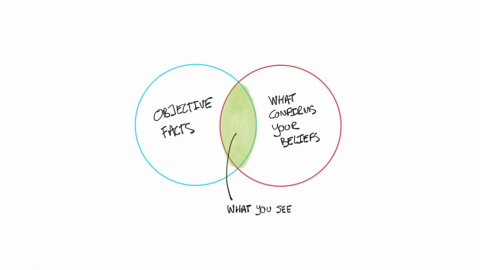

The problem with confirmation bias

Humans make decisions first and then do their research, and that's backward.

I should know. I fall into the following trap again and again.

1- I have an idea.

2- “Somebody Smart” questions the idea.

3- I call my friend, Jason.

4- Jason tells me it’s a good idea.

5- I say, “See, it’s a great idea!”

6- I carry out my great idea.

7- My great idea often turns out to be a bad idea.

8- Oh well, it was fun anyway.

9- “Somebody Smart” rolls his eyes.

10- Aaaand… repeat.

Academics have a name for this behavior: it’s called Confirmation Bias. You’ve probably heard of it. It’s the process of making a decision before we do our research. Not only do we put the cart before the horse, but when we actually get around to doing our “research,” it just consists of gathering evidence that supports what we’ve already decided and summarily dismissing everything that disagrees with us.

We all do this. And it’s an incredibly difficult habit to break. But that’s not to say impossible.

There is one way I’ve found to circumvent this behavior. I call it the Confirmation Bias Prevention Program. Here’s how it works.

1- Find someone who disagrees with a decision you’re about to make (an anti-Jason).

2- Ask them why they disagree with you.

3- Carefully listen to what they have to say. Listen, as Stephen R. Covey says, “with the goal to understand, not to be understood.”

4- Continue listening until you can honestly say, “I now understand why you believe that.”

That’s it, it’s that simple. This doesn’t guarantee you won’t do the thing you want to do… but that’s not the point. The point is to carefully and thoughtfully analyze the pros and cons of a decision so you can make it in an unbiased way. And the Confirmation Bias Prevention Program is a great step in that direction.

(Written by Carl Richards of behaviourgap.com)